How to Spot Debt Collection Scams

Why Debt Collection Scams Are So Common

Debt collection scams are on the rise, and they often sound convincing. Someone calls, texts, or emails you, says they’re a debt collector, and demands immediate payment, sometimes for a debt you don’t even recognize.

Knowing how to spot debt collection scams is one of the best ways to protect your money and your personal information. This guide explains what a debt collection scam looks like, the red flags to watch for, how to verify whether a debt collector is legitimate, and what to do if you suspect something isn’t right.

What Is a Debt Collection Scam?

A debt collection scam happens when someone pretends to be a debt collector or misuses debt collection tactics to trick you into paying money you don’t owe or to steal your personal information. These fake debt collectors may use the phone, text, email, or social media messages to create urgency and fear.

The Federal Trade Commission (FTC) describes “phantom debt collection” as cases where scammers try to collect on debts that either don’t exist, have already been paid, or don’t belong to you. They may pretend to represent a real company, law firm, or government agency, even though they have no legal right to collect anything from you.

Because real debt collectors also contact people about unpaid accounts, it’s critical to understand how to know if a debt collector is a scam before you share information or send any money.

Major Red Flags of a Debt Collection Scam

While scammers constantly change their scripts, many debt collection scams share the same warning signs. If you notice one or more of these, it’s a signal to slow down and verify everything before you act.

1. Threats of arrest or immediate legal action

One of the biggest red flags in a debt collector scam is a caller who threatens to have you arrested, jailed, or “picked up” by law enforcement if you don’t pay right away. Legitimate debt collectors do not have the power to arrest you and cannot threaten criminal charges over consumer debts.

The Consumer Financial Protection Bureau (CFPB) notes that threats of arrest, deportation, or criminal charges are classic scam tactics designed to scare you into paying without asking questions.

2. Pressure to pay immediately

Another common sign of a debt collection scam is intense pressure to pay right now. Scammers may say things like “you must pay within the hour” to push you into quick decisions.

Real debt collectors might discuss deadlines, next steps, or same-day payment; but they should still allow you to exercise your rights to dispute or request validation if you so choose.

3. Demands for unusual payment methods

If a supposed debt collector insists that you pay with gift cards, prepaid debit cards, cryptocurrency, or peer‑to‑peer apps, that’s a major red flag for a debt collector scam.

The FTC warns that scammers love these payment methods because they’re hard to trace and nearly impossible to reverse. Legitimate collectors typically offer more standard options, such as paying by check, card, or through secure online portals.

4. Refusing to provide written information or validation

Under federal law, most real debt collectors must send you information about the debt, often called a validation notice, either as their first communication or within five days of first communicating with you.

If someone refuses to provide any written details or won’t send a validation notice, that’s a strong sign you may be dealing with a fake and abusive debt collector rather than a legitimate one.

5. Refusing to give company details or contact information

The CFPB explains that to verify a debt collector, you should be able to ask for and receive basics like:

The collector’s name

The company’s name

A mailing address

A phone number

If the person on the phone won’t give you this information, becomes defensive, or hangs up when you ask for it, treat that as a warning sign of a debt collection scam and don’t share personal details.

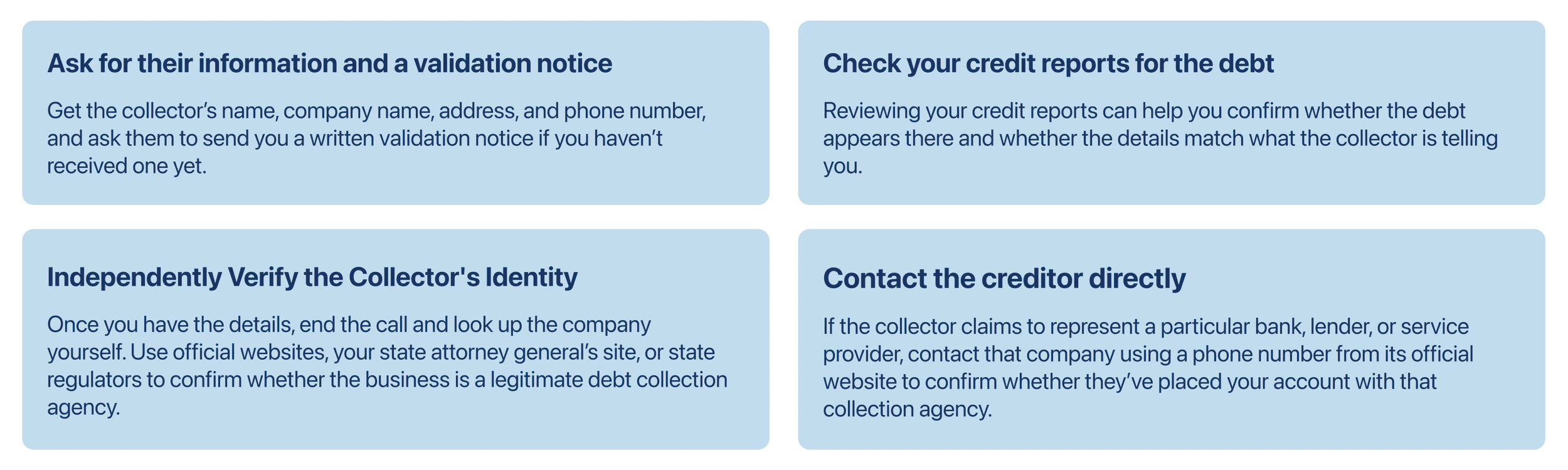

How to Verify If a Debt Collector Is Legitimate

Once you know the signs of a debt collection scam, the next step is learning how to check if a debt collector is real. Taking a few minutes to verify can save you from losing money or exposing sensitive information.

Here are practical steps you can take:

Resources explaining how to tell if a debt collector is legitimate or a scam provide helpful step‑by‑step guidance as you work through this process.

What to Do If You Suspect a Debt Collection Scam

If you think you’re dealing with a debt collection scam, the most important thing is to protect yourself and report what’s happening. Here are key actions to take:

Tell the caller you want everything in writing

Ask for a validation notice and say you will review it before making any decisions. Scammers often back off when they know you understand your rights.

Document the interaction

Write down the time, date, phone number, and what the caller said. Screenshots of texts or emails can also be useful.

Report the scam attempt

You can report fake or abusive debt collectors to:

Your state attorney general or state consumer protection agency

Consider placing alerts if you shared information

If you already gave out personal or financial information, consider placing fraud alerts on your credit files, monitoring your accounts, or consulting identity‑theft resources for next steps.

The FTC’s guidance on fake and abusive debt collectors and its alert on debt collection: know your rights, avoid scams provide more details about how to report and what protections you have.

Verify a Communication from Unifin

If you’ve received a call, text, letter, or email claiming to be from Unifin and you want to confirm it’s real, you don’t have to guess. You can safely verify a communication from Unifin by visiting Unifin’s official verification page and following the steps there to match your reference ID, creditor information, and contact details with what appears in Unifin’s secure systems.

The focus is on providing accurate information and secure, self‑serve options so you can review your account and choose a resolution path that works for you.