What Is a Third-Party Debt Collection Agency?

Why You’re Hearing from a Third-Party Debt Collector

If you’ve recently heard from a third-party debt collection agency, it’s completely understandable to feel unsure or even a little confused. Many people only learn about debt collectors when they’re already dealing with financial pressure, a life change, or a billing issue, which can make everything feel heavier than it needs to be.

This guide is designed to give you clear, straightforward, information about what a third-party debt collection agency is, how your account may have ended up there and what you can do next.

What Is a Third-Party Debt Collection Agency?

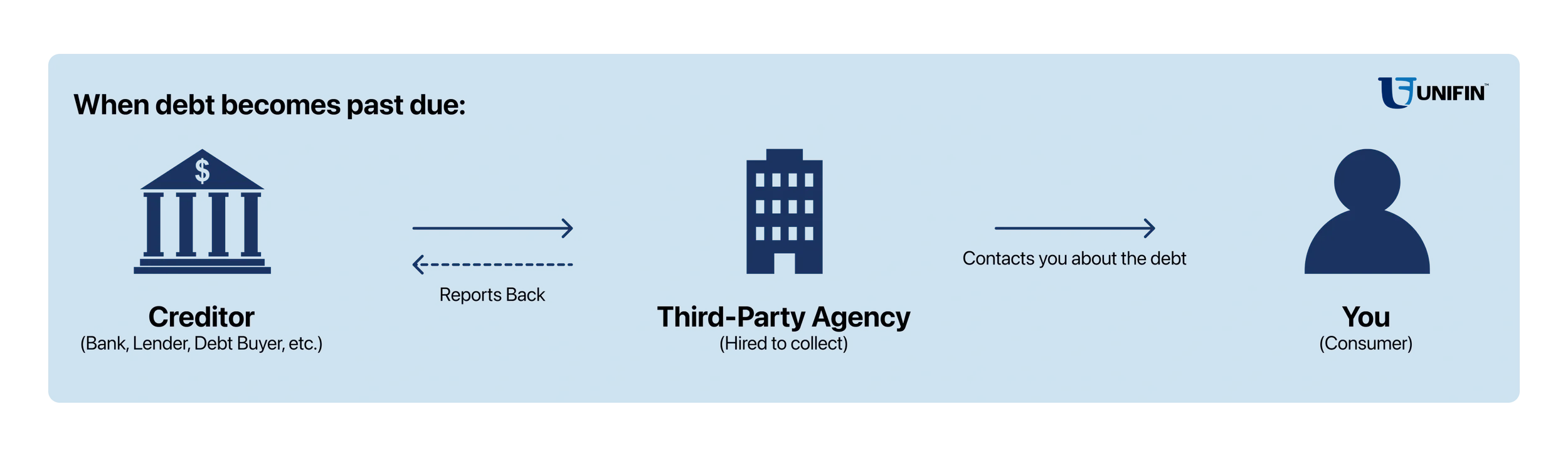

A third-party debt collection agency is a company that perform collection activities, on behalf of a creditor, on accounts that have fallen past due. In simple terms, they are a “third-party” because they are separate from both you (the consumer) and the creditor (the company to which the debt is owed).

Instead of handling collections on their own, many businesses turn to third-party agencies that specialize in communicating with consumers, explaining account status, and outlining possible ways to resolve past-due balances.

A third-party debt collection agency may be:

Working for the original creditor that still owns your account, or

Working for a debt buyer/current creditor that purchased your account from the original creditor.

Regardless of who currently owns the debt, the agency’s role is to communicate about the account, share information, and outline options to resolve the past-due balance over time.

Third-party debt collectors must follow federal and state laws that govern how they communicate with you and what they can and cannot do. In the United States, one of the key laws covering third-party collections is the Fair Debt Collection Practices Act (FDCPA), which sets rules to prevent unfair, deceptive, or abusive practices.

How Accounts Typically End Up with Third-Party Collectors

Most people don’t plan to work with a debt collection agency. It usually happens after an account has gone unpaid for a extended period of time, which can be caused by job changes, medical expenses, unexpected life events, or even something as simple as a missed bill or address change.

Here’s a clearer breakdown of how that process often works.

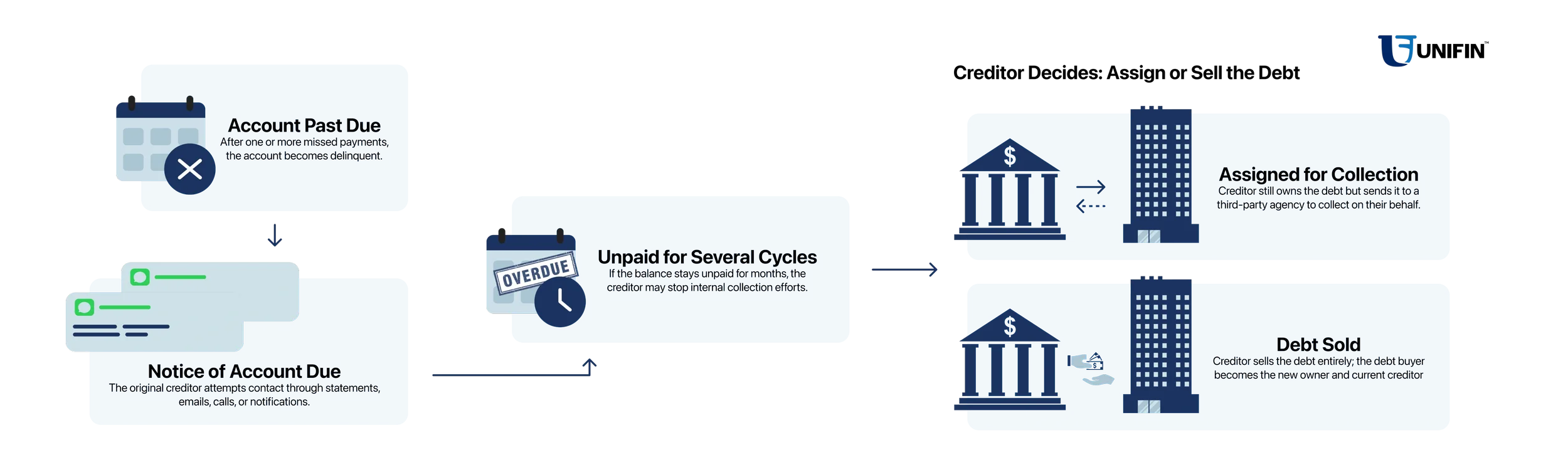

When an Account Becomes Past Due

When you miss one or more payments, your account becomes delinquent or past due according to your agreement with the creditor. At first, the company you originally owe will usually try to contact you directly through statements, emails, app notifications, or phone calls, to bring the account current.

If the account continues to go unpaid for several billing cycles, the creditor may decide that it makes more sense to involve a specialist than to keep trying to collect on their own. That’s where a third-party debt collection agency typically enters the picture; when the creditor assigns the account as a debt for collection with the third-party agency.

Why Creditors Use Third-Party Debt Collection Agencies

From the creditor’s perspective, working with a third-party debt collection agency can help ensure that accounts are handled consistently, efficiently, and in line with legal requirements. Agencies are set up specifically to manage:

Account outreach and communication

Required disclosures and notices

Record-keeping related to calls, letters, and agreements

Options like repayment plans or settlements, where applicable

For many consumers, this stage can actually bring more clarity to what’s going on. Instead of sporadic calls or confusing notices, you may receive more structured communication that clearly explains who the collector is, what the account is, and how you can respond.

What to Expect When a Collection Agency Contacts You

If your account has been placed with a third-party debt collection agency, you may be contacted in several ways. Agencies utilize communication channels allowed by law, such as letters, phone calls, and in some cases, emails or text messages if appropriate.

Early in the process, a legitimate agency should:

Identify itself as a debt collector

Provide the name of the original creditor

Share the amount owed

Explain why they are contacting you and how you can respond

Send you a written notice with key details (often called a “validation notice”) within a set period of time after first contact

Being contacted by a collection agency does not mean you are a bad person or that you’ve failed. It simply means your account is now being handled by a third party that is tasked with communicating about the debt and exploring potential next steps.

You always have the right to take a moment, read through the information carefully, and make sure you understand it before deciding what to do next.

How Modern, Digital-First Agencies Like Unifin Work

Not all debt collection experiences are the same. Traditional collection methods often relied heavily on phone calls and letters, which could feel stressful or confusing. Today, some agencies are updating this approach to better reflect how people actually live and manage money.

Unifin is an example of a consumer-focused, digital-first debt collection agency that aims to make the process more transparent and manageable. As a third-party collector, Unifin works with creditors to help consumers resolve past-due accounts, and does so through a mix of secure self-serve payment options, flexible arrangements, and empathetic, human-centered support.

In practice, this can mean:

Providing online portals where you can securely log in, see account details, and explore options 24/7

Offering flexible payment plans that better align with your actual budget

Communicating in clear, plain language, so you understand what’s happening and why

Focusing on clarity and choice, rather than pressure, to help you take the next right step for your situation

Third-party agencies play a role in helping creditors manage unpaid accounts, but you remain at the center of the process. You have the right to clear information, fair treatment, and time to understand your options before you decide what to do next.

If your account is with Unifin, know that the goal is not just to collect a balance, but to help you navigate the process with clarity, transparency, and choice. Unifin’s digital-first tools and flexible options are designed to support you in resolving past-due accounts in a way that feels more straightforward and less overwhelming.

If you’re ready to explore your options, you can visit Unifin’s secure payment portal or reach out to the support team to discuss flexible ways to move forward.